Skip to main content

Search

Search This Blog

Missy Bass

Loan Officer, NMLS# 912069

Pages

Home

About Me

More…

Posts

Showing posts from March, 2015

Show all

Posted by

Design By E

March 24, 2015

How To Be A Smart Buyer

Posted by

Design By E

March 17, 2015

Mortgages, Self Employment and What It Takes

Posted by

Design By E

March 11, 2015

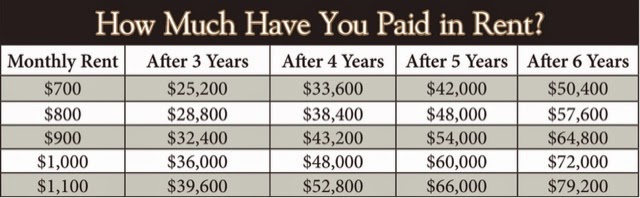

Rent Vs. Own. What's the better option?

Posted by

Design By E

March 03, 2015

DOs and DON’Ts while awaiting approval

Newer Posts

Older Posts

Home